High Tax Levies, Little Trust

How do companies perceive the German tax system? And what effect does it have on their day-to-day business and decisions? Those topics have now been investigated in a corporate survey conducted by researchers involved in the “TRR 266 Accounting for Transparency” collaborative research centre, consisting of Paderborn University, Humboldt University Berlin as well as Freie Universität Berlin. The answers provided by the 657 predominantly small and medium-sized companies throughout Germany, mainly in North Rhine-Westphalia (NRW) and Baden-Wuerttemberg, show that most respondents assess the tax burden and the associated tax-related administrative expenditure as comparatively high. Only very few trust the state to deal responsibly with the tax revenues.

Taxes are considered an important locational factor. Should the tax system seem too complex or if the taxes are considered to be too high or unjust, that can lead to repercussions for corporate action and thus, ultimately, for the economic situation. The TRR 266 corporate survey shows that it may well be expedient to take a closer look at the mood of German companies, as most of the 657 respondents are extremely critical of various aspects of the German tax system.

Lower taxes, more investments?

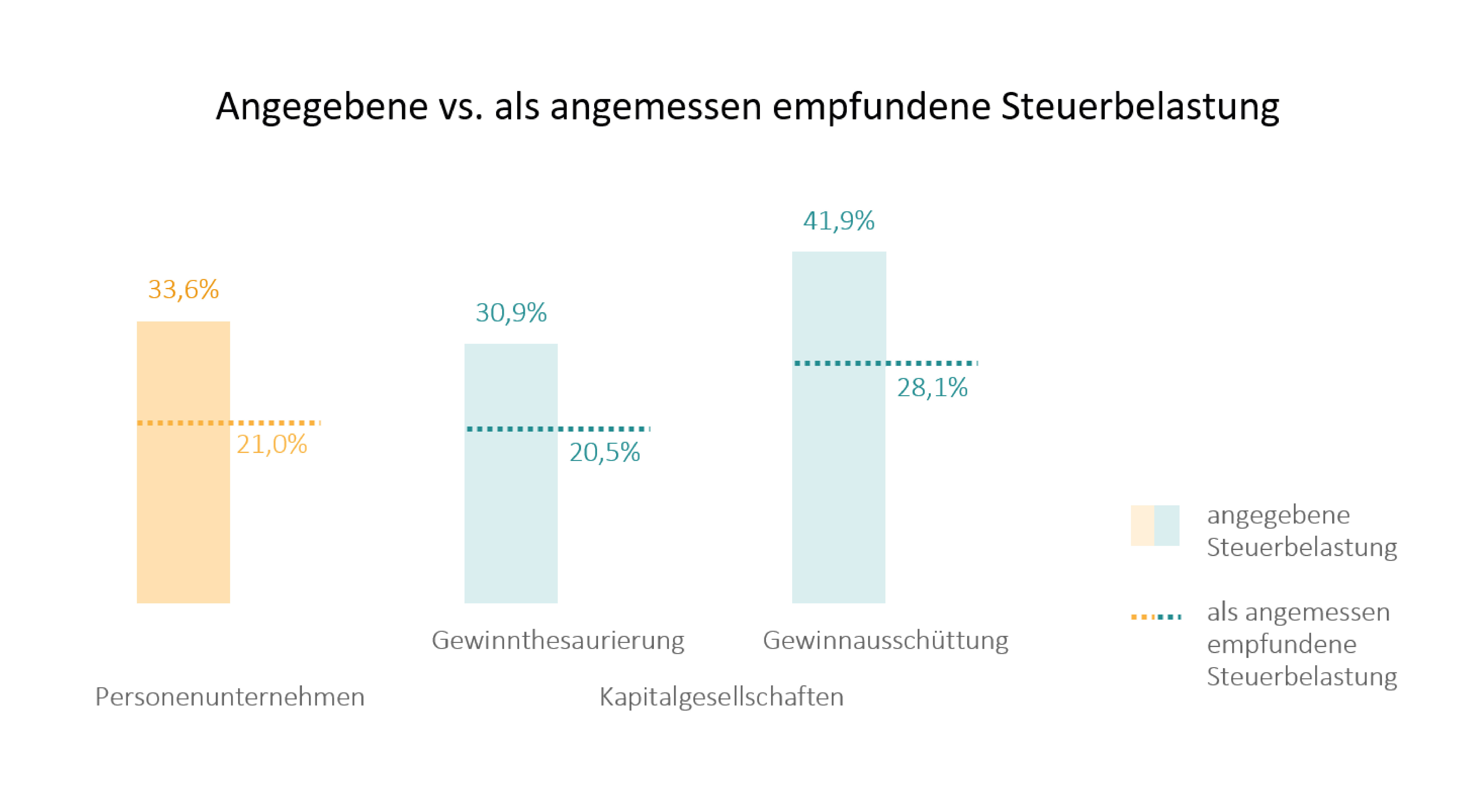

That includes the amount of tax levies. On average, the respondents estimated the corporate tax burden at around 36 percent. The amount they consider reasonable is significantly lower – around 23 percent on average. Around 75 percent of the respondents also take the view that they pay more taxes than foreign competitors. Prof. Caren Sureth-Sloane of Paderborn University explains: “This relatively large discrepancy between the reported tax burden and the tax burden considered reasonable naturally makes us sit up and take notice. After all, decisions are influenced by perceptions. For example, a tax burden considered to be too high could cause companies to make fewer investments.”

Most of the respondents stated that a reduction in the tax burden would promote their own investment activity. Tax reductions thus occupy 2nd place in the list of the most important investment-promoting measures, closely followed by an investment deduction. Special depreciation occupies 1st place with the majority of respondent votes. According to Prof. Ralf Maiterth from Humboldt University Berlin, “These results are interesting. After all, investments are an important tool for improving the economic situation – especially in times of crisis such as the current coronavirus pandemic.” Also of probable interest in this context is the fact that some respondents say their investment activity is being impeded by the high tax-related administrative expenditure.

Complex tax system, high administrative expenditure

Irrespective of legal form and corporate size, the tax-related administrative expenditure constitutes a significant burden on the day-to-day business life of many of the respondents. On average, the percentage of tax-related administrative expenditure is estimated to be around a third of the entire in-house bureaucratic expenditure. A significant majority of companies cite the duties to provide proof and supporting documentation, followed by the preparation of tax returns and invoicing pursuant to the Turnover Tax Act, as well as the calculation and levying of income tax as essential drivers.

Companies are also very critical of the complexity of the tax system. A significant 90-percent majority considers the German tax system to be too complex. Just 20 percent of respondents view this complexity as being necessary to enable differentiated corporate taxation on a case-by-case basis. 70 percent of companies are dissatisfied with the information provided by the financial supervisory authorities in conjunction with tax-related issues.

Very little trust in state action

Most respondents also expressed mistrust vis-à-vis the way the state deals with taxes: 80 percent of the respondent companies doubt that the state deals responsibly with tax revenues. According to the researchers, this is a clear vote of mistrust that should not be taken lightly. According to Maiterth, “A lack of trust in the state and tax system is bad for this country’s economy and social climate.” Sureth-Sloane adds: “In our capacity as mediators between practice and politics, we hope our research will contribute to restoring this trust – by revealing discord and misperceptions, identifying causes and showing potential solutions.”

The executive summary of the survey results can be viewed at: https://www.accounting-for-transparency.de/wp-content/uploads/2021/07/trr266_b08_executive_summary_steuerliche_belastung_2021.pdf

Information on the study

Prof. Martin Fochmann (Freie Universität Berlin), Vanessa Heile (Paderborn University), Hans-Peter Huber (Humboldt University Berlin), Prof. Ralf Maiterth (Humboldt University Berlin) and Prof. Caren Sureth-Sloane (Paderborn University). Steuerliche Belastung deutscher Unternehmen – Steuerlast und Verwaltungskosten (Tax burden of German companies – Tax burden and administrative costs) – Executive Summary

Background information

The “TRR 266 Accounting for Transparency” collaborative research centre was launched in July 2019 and is initially being funded for four years by the German Research Foundation (DFG). It is the first collaborative research centre focusing primarily on business administration topics. Around 80 scientists from eight universities are involved in the collaborative research centre: Paderborn University (coordinating university), Humboldt University Berlin and University of Mannheim, as well as researchers from LMU Munich and ESMT Berlin, Frankfurt School of Finance & Management, Goethe University Frankfurt, and WHU - Otto Beisheim School of Management. The researchers are investigating how accounting and taxation influence corporate transparency and what effect regulations and corporate transparency have on the economy and society. The funding volume for the collaborative research centre stands at around EUR 12 million.

![[Translate to English:]](/fileadmin/_processed_/8/5/csm_Pressemitteilung_vorschaubild_702c9bfadb.jpg "[Translate to English:]")

{kind=link}

{kind=link}